‘Renewing Britain’ by failing homeless children

In one of the world’s richest countries, 165,500 British kids live in ‘temporary accommodation’.

I have been working with Shelter, the homeless charity, over the last few months to build up the case for public investment in social housing.

In her Spending Review Statement this week the Chancellor Rachel Reeves dashed our hopes, ignoring the fates of thousands of homeless children and their families.

In this post and the next, I want to grumble (all over again) about politics/economics here in Britain; but in the next post explore a c-r-a-z-y issue with you: one that I have tried hard to avoid. An issue central to the Trumpian project. I refer to the fantastical and criminal world of Stablecoins; Trump and Musk’s Genius Act; and the creation of 8,000 crypto currencies. (I kid you not). We can no longer dismiss the world of crypto as irrelevant to the global economy, because Silicon Valley oligarchs are set on using the wealth they’ve accumulated to fulfil a dangerous mission: one actively supported by the American president.

Their aim is to use a flawed, corrupt concept of money to transform the US monetary system and destroy its regulatory institutions. Those actions will have a massive impact on the rest of the world “given the hegemonic role of the US since the second world war” as Martin Wolf notes in his latest column.

The crypto revolution threatens chaos.

That post will follow soon. But first:

Chancellor Rachel Reeves: ‘Renewing Britain’ by failing homeless children

I have been working with Shelter, the brilliant homeless charity over the last few months to build up the case for public investment in public, low-rent housing, otherwise known as social housing. I argued that:

England is facing the worst housing emergency since the Second World War. The number of children in temporary accommodation has reached yet another record of 165,500, while local authorities are on the brink of collapse, spending three times more on temporary accommodation than a decade ago, with a further rise of 71% projected by the end of this Parliament if nothing changes.

I went on to explain how the building of public, social housing could be financed:

As Keynes taught, public investment at a time of private sector weakness drives both private and public investment, employment, income and tax receipts. If targeted at the creation of new assets that are revenue generating, the spending will pay for itself.

Social housing is a prime example. Shelter's call for the creation of 90,000 new public assets – social rent homes – a year, costing just over 1% of GDP, would not only address urgent need, but would create hundreds of thousands of jobs, boost private supply chains and generate tax revenues.

Kept as assets on the state's balance sheet, the social housing stock will continue to reduce public debt.

Furthermore, investment in housing would increase the skills, the stability and the mobility of labour. Research shows such investment would begin returning a profit to the Exchequer within 11 years, while reducing demand for housing benefit and temporary accommodation.

All that may have been to no avail. Shelter’s heroic efforts to help rescue 165,500 children from the immiseration brought on by homelessness, appear fruitless in light of Chancellor Rachel Reeves’s recent statement to the House of Commons. She was

proud to announce the biggest cash injection into social and affordable housing in 50 years with a new affordable homes programme in which (she said) I am investing £39 billion over the next decade—direct Government funding that will support house building, especially for social rent.

Shelter’s Mairi MacRae, Director of Campaigns and Policy called the Chancellor’s statement…

“..a watershed moment in tackling the housing emergency. It’s a huge opportunity to reverse decades of neglect and start a bold new chapter for housing in this country. To truly tackle rising homelessness, it must come alongside a clear target for delivering social rent homes.

In fact, the Chancellor has agreed only meagre sums to be allocated (i.e. to subsidise) even more private ‘affordable housing’ - not public, low-rent, social housing, built to decent standards. The HMT Spending Review statement on housing (filed under Chapter 4. Growth and Clean Energy of the Spending Review) makes her intention crystal clear:

£39 billion for a new 10-year Affordable Homes Programme;

Catalysing additional private investment to further boost house building by confirming £4.8 billion in financial transactions (FTs) from 2026-27 to 2029-3

Is the phrase ‘catalysing additional private investment’ just another way of saying the taxpayer is ‘de-risking’ private investment in housing?

The Institute of Fiscal Studies’s associate director, Ben Zaranko, writing in the Financial Times of the 12th June explained how meagre was this allocation of public resources.

The small print suggests spending of about £3bn a year over the next three years, which is not a million miles away from what is currently spent on the AHP (Affordable Homes Programme).

This is why enormous-sounding numbers should always merit further scrutiny…

To confirm our suspicions, the government refused to spell out the breakdown of annual expenditure of the new AHP settlement to the Financial Times. In other words, we are not told how much of it will go to social housing as opposed to ‘catalysing additional private investment’ and the private construction sector’s ‘affordable housing’ schemes.

That is a huge disappointment and a betrayal of all those homeless children living in ‘temporary accommodation’. No surprise there.

As we argued in the Shelter piece:

Britain's current policy is to prioritise day-to-day spending on private market subsidies over capital investment in public assets. No wonder the housing benefit bill has surged, transferring public money into inflated private rents and landlords, rather than in long-term, income-generating public assets.

The refusal by successive governments to invest in social housing is due in part to a persistent misreading of the role of public finances in stimulating both public and private economic activity. From 2010 onwards, political leaders chose austerity over investment, despite historically low interest rates, spare capacity and ample fiscal space. The results are now painfully clear: a weakened economy and its inevitable counterpart, the budget deficit, compounded by spiralling housing benefit costs, rising private rents, growing inequality, and stagnant productivity.

Nevertheless, I expressed some sympathy for the Chancellor. This was my reasoning. The Bank of England not only fails to support the objectives of her democratically elected government, its staff actively work against government policies. By doing so, the Bank ignores its mandate under Part 2, Section 11 of the 1998 Bank of England Act. That mandate instructs the Bank

to maintain price stability, and, subject to that, to support the economic policy of Her Majesty's Government, including its objectives for growth and employment.

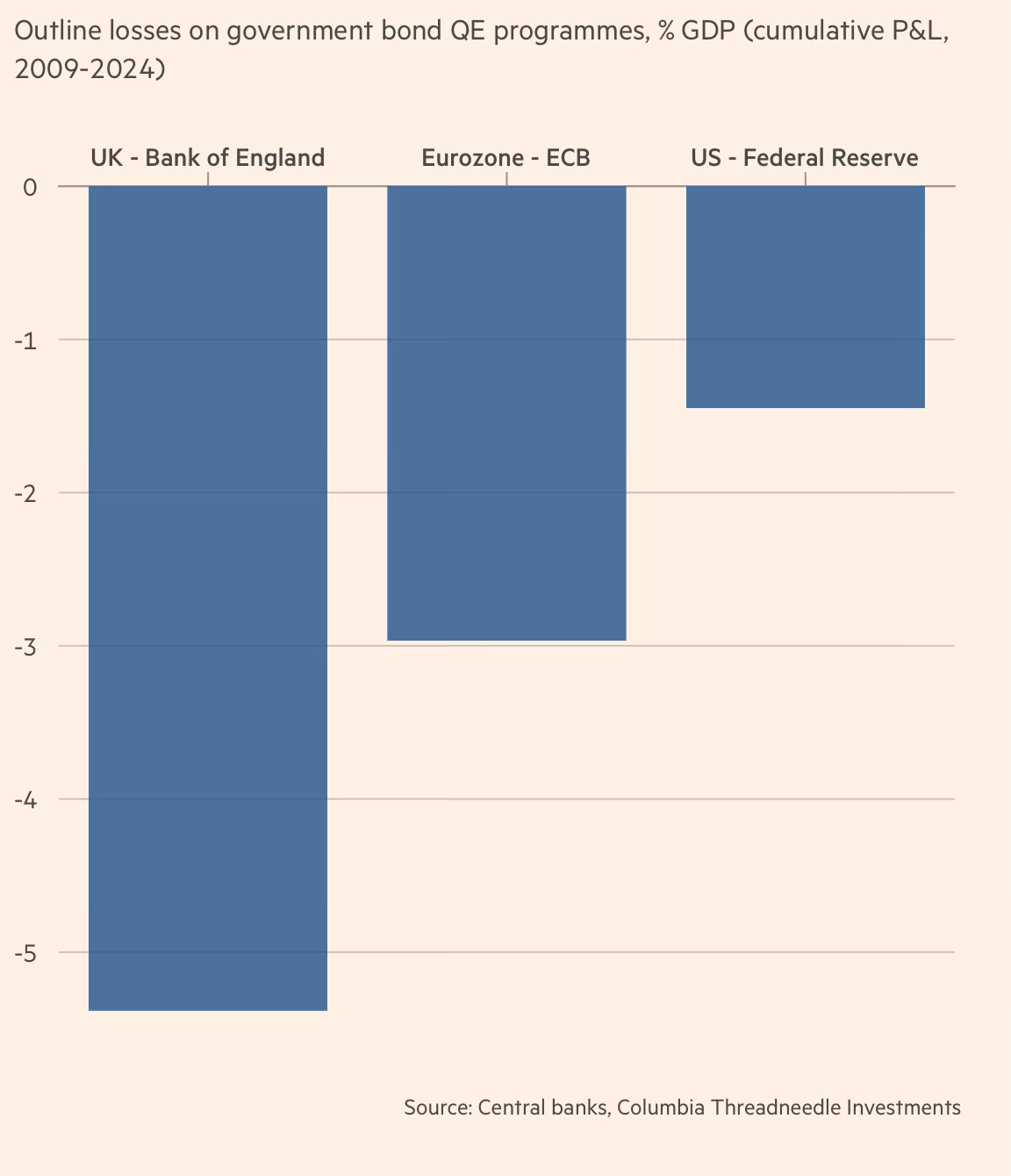

Fiscal and monetary policy applied by two of the government’s most important public institutions - the Treasury and the nationalised Bank of England - conflict, and in fact, are opposed. Treasury intransigence is matched by the Bank of England's aggressive use of Quantitative Tightening to burden the government with costs amounting to £20 billion over 2.5 years. In other words, monetary policy is actively interfering in, and undermining fiscal policy.

Monetary policy cancels out much of what fiscal policy works to achieve. Deliberately. High real rates of interest (that have had little impact on inflation) make both government and private borrowing prohibitive. Quantitative tightening dumps the Bank of England’s QE losses on to the Treasury, worsening the fiscal balance. As Christopher Mahon argues, the Bank’s QE losses far exceed those of other central banks:

Mahon and his team highlight the implications for fiscal policy of the Bank’s Quantitative Tightening (QT) policy:

the BoE being a large seller of gilts had pushed yields up. We put the cost to the Treasury from the higher debt servicing costs at around £1bn per year.

The Bank of England complains that the reason rates are high is because British workers are succeeding in maintaining their living standards. According to the Guardian Huw Pill (the Bank of England’s chief economist) complained

that the structure of the UK labour market was becoming less flexible, giving employees the power to maintain their living standards through higher pay.

After years of stagnant wage growth and a prolonged cost-of-living crisis, civil servants at the Bank of England are actively opposed to British workers striving to maintain their living standards.

Given the Bank’s high rates of interest, it is no wonder that both public and private investment is lower in Britain than in most G8 economies. It should not come as a surprise therefore that

the UK economy suffered its worst monthly contraction in April since 2023 with a GDP decline of 0.3% as the Financial Times reports.

It’s enough to make one despair. But wait, there is good news.

In a rare bright spot, the construction sector recorded growth of 0.9 per cent, helped by unusually sunny weather…

…and years of public subsidies.

When the BoE puts the problem down to the population "maintaining its living standards" it is difficult not to frame this as a deliberate policy to increase inequality. The alternative is to believe that they don't have a real handle on how economies work. Not being a fan of black and white answers I suspect the truth is almost certainly both.

Huw Pill seems firmly committed to the most conservative of policies. The country can only succeed by the poor getting poorer. He is consistent.

On housing, 2 possible aspects of social housing that do not get a mention. As well as providing affordable housing for the poorest, they enabled others to save and perhaps buy places of their own. And they also provided a degree of competition for private sector rentals.