Beyond Growth: A Strategy for Tackling Power. My speech to the EU Conference

On the need to blow up the 'easy money' pipeline

Ten days ago I addressed a thousand delegates (and many more online) at a conference organised by Members of the European Parliament (MEPs). The theme was ‘Beyond Growth’ - and the conference was sponsored by MEPs representing Green, Left, but also Conservative parties.

The theme of my panel was ‘The Power of Economic Models’. Speakers were only given ten minutes and I had a great deal to pack in, so there is much ‘shorthand’ in the speech, and in the notes published below…

There was controversy at the event around the concept of ‘economic growth’. Most delegates favoured ‘degrowth’ and heckled MEPs concerned to end ‘fossil fuel-led growth’ - but keen to promote ‘economic growth’ by which they meant (in my view) more investment, employment and pay for their constituents back home, in the new green economy.

This conflict between what can broadly be defined as the green movement and those concerned to defend ‘green investment jobs and pay’ is a fissure caused by the economic concept of exponential ‘growth.’ It is a fissure that must be bridged by the climate change movement if we are to mobilise the majority for transformative change. It’s an issue I face as a member of the Scottish government’s Just Transition Commission when sitting around a table with trades unionists representing oil rig workers as well as environmentalists to discuss the re-structuring and transformation of the Scottish economy. An issue I will tackle in my next post..

You can watch the EU speech here - the notes are below.

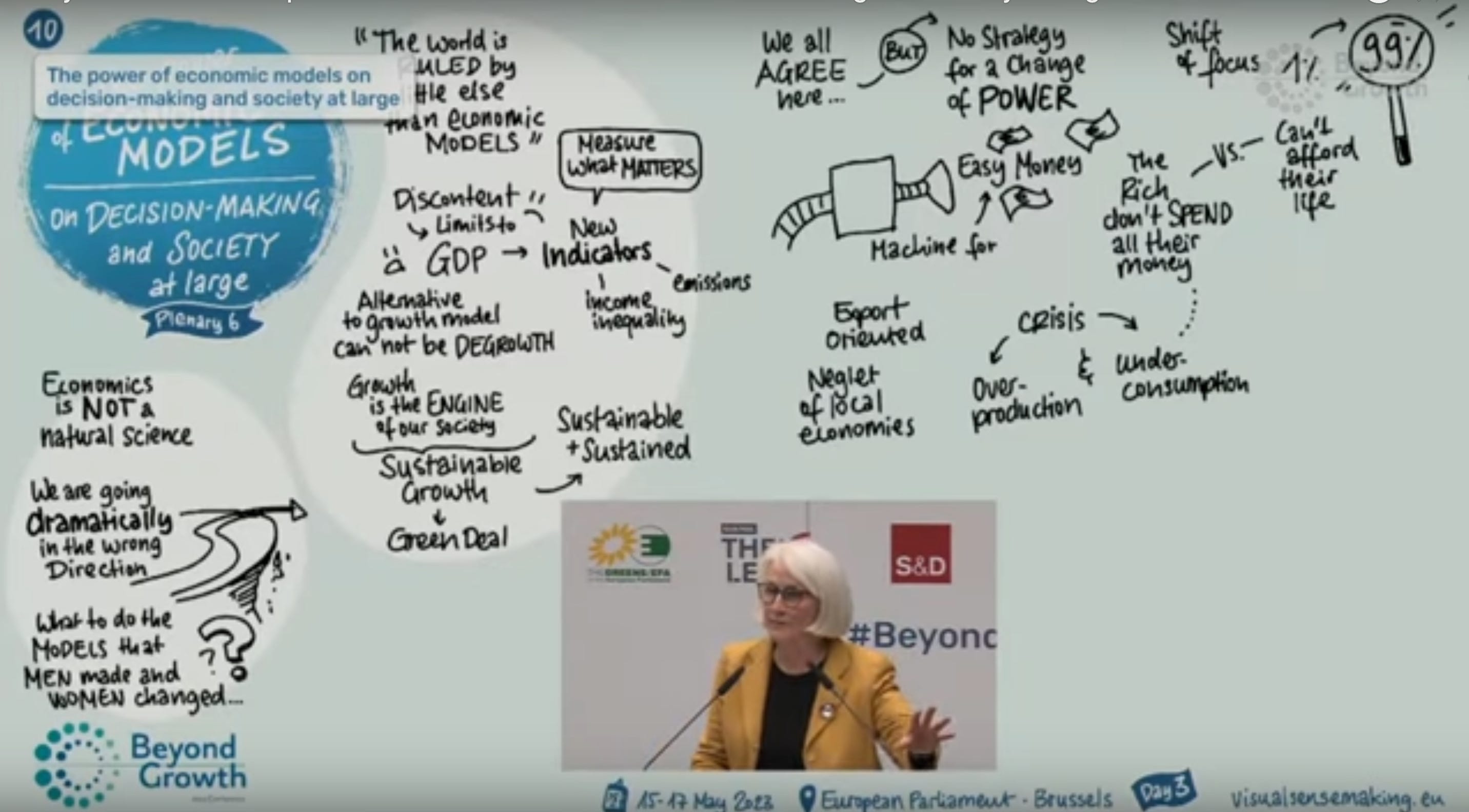

The Power of Economic Models

Thanks are due to MEPs that organised this event, and their excellent staff teams.

Thanks are also due to the President of the Commission, Ursula von der Leyen for her support for the conference. Her speech, and her statement that the “a model of growth based on fossil fuels is now obsolete” was in my view, highly significant. The green movement does not have enough friends. Instead of boo-ing and heckling we need to welcome all those that take steps toward us.

We have spent three days basking comfortably in consensus. And feeling good about ourselves.

We all agree on the need for Sufficiency, Equity, Well-being, a Regenerative Economy, a Donut Economy and a Circular Economy.

But there has been no discussion of a strategy for challenging power.

There are two sites of power we must challenge:

The Fossil Interest

And

The Money Interest.

Both have erected barriers and barricades to our challenges. And while we have protested and booed and mobilised public opinion against the Fossil Interest, we have neglected the Money Interest.

The Money Interest is where real power over the planet lies.

Toxic emissions are the outcome of ‘easy money’ poured into the Fossil sector. To stop emissions we need to stop the flow of largely unregulated credit into fossil fuels.

The Money Interest has something resembling a gas pump, a giant tap or spigot that pours out unregulated credit, from both commercial banks and also the ‘shadow banking’ sector - the sector that operates in the financial stratosphere – beyond the reach of regulatory democracy.

To save the planet we need to switch off that ‘easy money’ gas pump. We need to focus on monetary policy, not fall into the trap set by the Money Interest of focusing exclusively on fiscal policy.

To challenge the power of the Money Interest, we need to understand the global economic model - ‘Capitalism without Brakes’ - to quote Jim Rutt.

Capitalism without Brakes is powered by infinite supplies of largely unregulated credit.

‘Easy Money’

The global dominant economic model – the theme of this panel - orients economies away from the domestic sphere, towards exports, as Matt Klein and Michael Pettis argue in their important book, Trade Wars are Class Wars.

The export orientation of economies like Germany and China boosts the income of the 1% - the corporations that are exporters, while depressing the incomes of the 99% - wages of workers at home, in the domestic economy. Germany since the Hart reforms is the classic example, but so is China.

But here is the thing – the 1% - the rich – don’t spend all they earn. There are limits to the number of super yachts, private jets and big houses they can buy. There are limits to the number of rockets Elon Musk can explode.

In contrast, the 99% - the workers – spend all their income. On keeping a roof over their heads, buying food, maintaining health, and sending their kids to university. But their incomes are falling in real terms, so they don’t have the purchasing power to buy all that is produced by the export-oriented economy.

Far from society’s purchasing power chasing too few goods and services, we have too many goods and services chasing too little money.

This leads to high levels of debt, as the 99% borrow to keep the roof over their heads, pay for health services etc, and as firms borrow because they can’t sell all that they produce, so sales fall.

The consequence is over-production, high levels of debt and falling incomes. The reverse of much commentary - a crisis of over-production and under-consumption.

And that, as we know from experience, leads to global financial crises.

Another financial crisis is inevitable, although predicting its timing is tricky.

What lessons does this economic model hold for the green movement?

First, we must stop attacking and blaming the 99% for excess consumption. Instead we must attack the 1% - the rich – for excess production, powered by excessive ‘easy’ largely unregulated money.

As Phillippe Lamberts has said, “This is a fight. A struggle. Even a war – to defend the planet.”

How do we mobilise the 99% to break down the barricades erected by the Money Interest? It is important to remember what Karl Polanyi taught us…

That when governments refuse to protect the interests of the majority, instead leaving everything to the ‘invisible hand’ of the market…

And when governments argue they are helpless and “it’s the market” causing impoverishment etc (in housing, food and education)…

Then people look for someone, an institution that will protect society from the market. They turn to the ‘protection’ offered by ‘strongmen’ - and women (in the case of Italy).

This is why we have the rise of authoritarianism - so-called strong men and women who promise to protect society from the depradations of ‘the free market’.

To mobilise the majority for a progressive project, the first steps we can take are these:

Shine a very bright light on the the giant spigot of the finance sector.

Second, educate ourselves. Finance, monetary policy is not rocket science. If I can understand it, so can you.

Third, we need to understand that the Money Interest – the 1% - based on Wall St., Frankfurt and the City of London, would not have the wealth they enjoy without the public infrastructure – the ‘plumbing’ - supplied by institutions and services maintained and provided by taxpayers:

The central bank – which periodically bails out the sector

Government bonds – safe assets for investors

And the annual income streams from taxpayers – stretching decades into the future

Income streams that are the very profitable, safe ‘rents’ on government bonds.

We need to acknowledge and deploy the power embedded in public institutions and funded by taxpayers.

We need to demand tougher terms and conditions for their use by private finance.

And finally, we need to mobilise public opinion and political power – by focusing on the 1%, not the 99%.

To echo Andreas Malm, We need to blow up the ‘easy money’ pipeline.

Thank you.

Watch the full plenary here

Music to my ears. In my ninth decade you are helping bring some clarity to my understanding of political economy.

Once the public understands that government deficits are equivalent to the public surplus and that the public surplus is largely held by 1% of the population, the correlation between the deficit and wealth inequality will become evident.